“Unlock the Benefits: Understanding Health Insurance in the USA with 10 Essential Insights”

"Navigate the complexities of health insurance in the USA with these ten essential insights, empowering you to make informed decisions about your coverage."

Navigating health insurance in the United States can be complex due to various plans, regulations, and terminology. Understanding how it works is crucial for ensuring you have the coverage you need. Here are ten essential insights into health insurance in the USA.

1. What is Health Insurance?

Health insurance is a contract that provides financial coverage for medical expenses in exchange for monthly premium payments. It helps cover costs for doctor visits, hospital stays, surgeries, and prescription medications.

2. Why Health Insurance is Crucial

Financial Protection

Unexpected medical expenses can quickly accumulate. Health insurance acts as a safety net, helping to cover significant costs associated with healthcare.

Access to Care

With health insurance, you are more likely to seek preventive care, which can catch health issues early and improve outcomes. Insured individuals generally have better access to a wider range of healthcare services.

Peace of Mind

Having coverage allows you to focus on your health without the constant worry of potential medical bills, making it easier to seek care when needed.

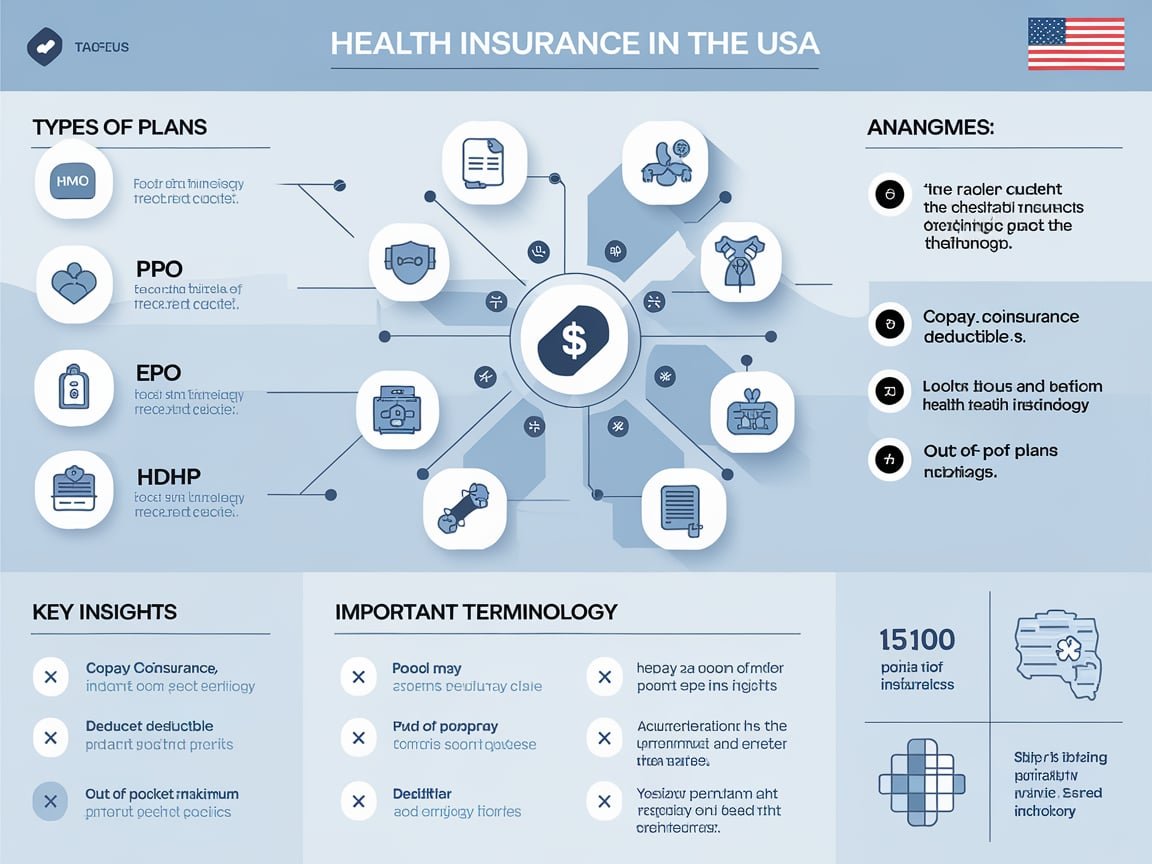

3. Key Terms to Know

Understanding common health insurance terminology can help you make better decisions:

- Premium: The monthly payment you make for your health insurance policy.

- Deductible: The amount you pay out-of-pocket before your insurance begins to cover costs.

- Copayment (Copay): A fixed fee you pay for specific services at the time of your visit.

- Coinsurance: The percentage of costs you share with your insurer after meeting your deductible.

- Out-of-Pocket Maximum: The maximum amount you will pay for covered services in a plan year; after reaching this limit, your insurer covers 100% of costs.

4. Types of Health Insurance Plans

In the USA, several types of health insurance plans cater to different needs:

- Health Maintenance Organization (HMO): Requires you to choose a primary care physician (PCP) and get referrals to see specialists. Generally has lower premiums and out-of-pocket costs.

- Preferred Provider Organization (PPO): Offers more flexibility in choosing healthcare providers and does not require referrals for specialists. Typically has higher premiums.

- Exclusive Provider Organization (EPO): Covers only in-network providers (except in emergencies) and usually has lower premiums than PPOs.

- Point of Service (POS): A hybrid plan that requires referrals for specialists but allows some out-of-network coverage.

- High Deductible Health Plan (HDHP): Features lower premiums and higher deductibles, often paired with Health Savings Accounts (HSAs) for tax-free medical expenses.

5. Enrollment Periods

In the USA, enrollment in health insurance typically occurs during specific times:

- Open Enrollment Period: A designated time each year when you can enroll in or change your health insurance plan, usually in the fall.

- Special Enrollment Period: Allows enrollment outside the open enrollment period due to qualifying life events such as marriage, childbirth, or loss of other coverage.

6. Understanding the Affordable Care Act (ACA)

The Affordable Care Act (ACA), enacted in 2010, brought significant changes to health insurance in the USA, including:

- Mandatory Coverage: Most Americans are required to have health insurance or pay a penalty (though the penalty has been eliminated in many states).

- Subsidies: The ACA provides subsidies to help lower-income individuals and families afford insurance through the Health Insurance Marketplace.

- Coverage for Pre-existing Conditions: Insurers cannot deny coverage based on pre-existing health conditions.

7. Tips for Choosing a Health Insurance Plan

When selecting a health insurance plan, consider these factors:

- Assess Your Needs: Reflect on your medical history and anticipate your healthcare needs to find a plan that fits.

- Compare Plans: Look at various plans, focusing on premiums, deductibles, and out-of-pocket costs.

- Check Provider Networks: Ensure your preferred doctors and hospitals are in-network to avoid higher costs.

- Review Coverage Details: Understand what services are covered, including preventive care and prescription drugs.

- “Visit HealthCare.gov for more information on health insurance options.”Click here

8. Utilizing Preventive Care

Most health insurance plans cover preventive services at no cost, such as:

- Annual check-ups

- Vaccinations

- Screenings (e.g., mammograms, colonoscopies)

Utilizing these services can help you maintain good health and catch potential issues early.

9. The Importance of Keeping Your Plan Updated

Health insurance plans can change annually, so it’s crucial to review your coverage each year during open enrollment. Make sure your plan still meets your needs and check for any changes in costs or covered services.

10. Seeking Professional Guidance

If you’re feeling overwhelmed by the choices, consider consulting a licensed insurance broker or a healthcare advisor. They can help clarify your options and guide you in making informed decisions.

Conclusion

Understanding health insurance in the USA is vital for protecting your health and financial future. By familiarizing yourself with key terms, types of plans, and enrollment processes, you can navigate the complexities of health insurance with confidence. For more information and resources, visit HealthCare.gov to explore your options and find the coverage that’s right for you.